Navigating Mental Health Coverage: Understanding Insurance Basics

Understanding insurance can be a challenging task, especially for patients who are already dealing with a lot of stress and anxiety. However, it is essential to have a good understanding of how insurance works to make the most of your mental health benefits and receive the treatment you need.

In this post we will talk about:

Understanding key Insurance terms

understanding your out of pocket cost

WHAT TO LOOK FOR WHEN SHOPPING FOR AN INSURANCE PLAN

& give you helpful cheat sheet/Work Sheet

Insurance is a contract between you and your insurance provider that helps you pay for the costs of your healthcare. When you enroll in a health insurance plan, you pay a monthly premium, which is the amount you pay for your insurance coverage. In exchange, your insurance provider agrees to cover some or all the costs of your healthcare.

When you visit a healthcare provider or receive medical treatment, your insurance provider will be billed for the services provided. The amount that your insurance provider pays for these services will depend on your insurance plan, as well as the specific services provided. At New Life Counseling we can only bill insurance companies that we are In-Network with. If we are considered Out-of-Network we can provide you with a superbill that you can submit; you may be able to get a reimbursement from your insurance for some of your out of pocket costs.

There are several terms you should know when it comes to understanding your out of pocket costs for mental health services:

- Deductible: This is the amount you pay for your healthcare before your insurance coverage kicks in. For example, if your insurance plan has a $1,000 deductible, you will be responsible for paying the first $1,000 of your healthcare costs before your insurance provider begins to cover the costs. Your copay or co-insurance may or may not apply towards your deductible. Occasionally mental health costs, like a doctors visit, aren’t subject to a deductible- if that’s the case you may only owe the copay or co-insurance until your out of pocket max is met.

- Co-pay: This is a fixed amount you pay each time you visit a healthcare provider. For example, you may have a $20 co-pay for each visit to your primary care physician.

- Co-insurance: This is the percentage of the cost of healthcare services that you are responsible for paying after you have met your deductible. For example, if your insurance plan has a 20% co-insurance requirement and a healthcare service costs $100, you would be responsible for paying $20.

- Out-of-pocket maximum: This is the maximum amount you will be responsible for paying for your healthcare services in a given year. Once you have reached your out-of-pocket maximum, your insurance provider will cover the remainder of your healthcare costs for the year.

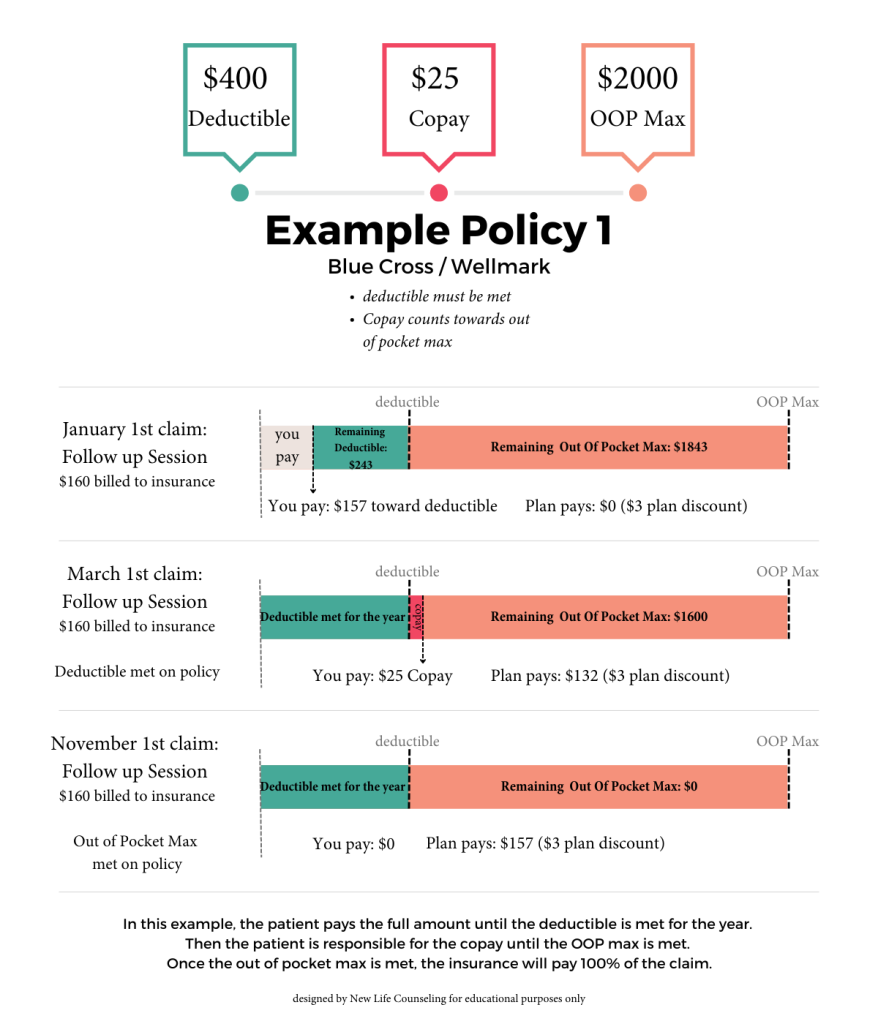

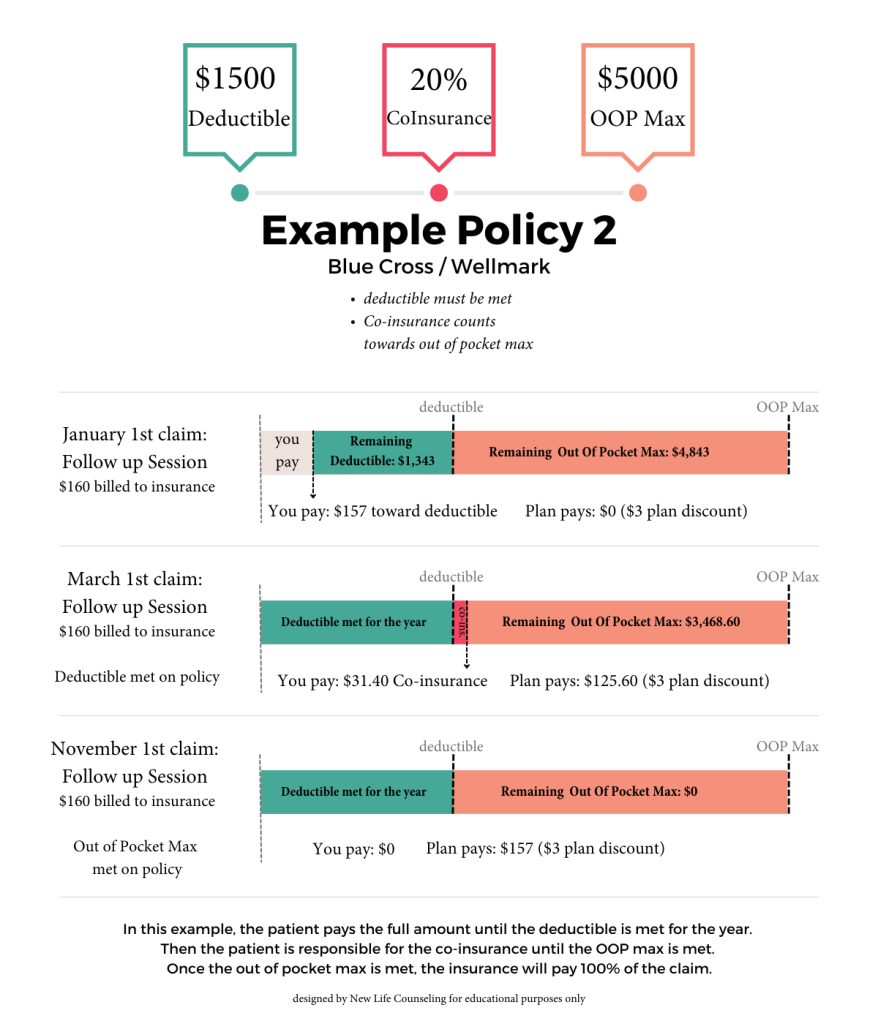

Here are a couple examples of policies where the mental health benefits are subject to the deductible: (click to view larger)

These are the kinds of details you will need to verify with your insurance member services. Most major insurances also have online portals where you can view your up to date remaining deductible and out of pocket max amounts.

Check out this helpful work sheet that will help you know what your out of pocket costs will be for your counseling sessions at New Life Counseling.

What if I have a really high deductible that I won’t meet?

If you don’t think you will be able to meet your high deductible we recommend you go with our cash pay prices. We discount our fees for cash pay or non-insurance patients (also called private pay or self pay). This means we will bill you directly instead of billing your insurance.

We do offer payment plans, and we have a few providers who offer sliding fee scales. You can view our cash pay prices here.

What if I have 2 insurance policies?

Sometimes people have two insurance policies. If so, one will be considered the primary and the other will be the secondary. There are some important things to understand about having multiple insurance policies:

- We must bill the primary insurance first so it is really important that you know which insurance is primary and which is secondary.

- Both insurance companies need to know about the other one. This is called Coordination of Benefits. If the primary discovers you have a secondary, they may send you a letter asking you to verify the secondary insurance details. If you don’t respond they will deny all claims until you call them, and you will be financially responsible for those denied claims.

- If we are out of network (do not take) your primary insurance we will not be able to bill your secondary insurance.

- If we are out of network for your secondary insurance, we can bill your primary and will simply not bill the secondary. You would be financially responsible for whatever balance the primary does not cover. You can submit a receipt to the secondary and they might reimburse you based on your out of network coverage.

How is Mental Health Coverage required by Law?

When it comes to mental health treatment, it is important to understand that most insurance companies are required by law to offer the same level of coverage for mental health services as they do for other medical services (2008 Federal Parity Law). The parity law doesn’t require insurers to provide mental health, rather it states that the mental health coverage can’t be more restrictive than physical health benefits. Most major insurance companies already have mental health coverage and the Affordable Care act requires that insurance exchange plans cover mental health and substance-use services.

This means that you should have some coverage for mental health evaluations, therapy, and medications, and that your copay or co-insurance amount should be equal to typical doctor office visits. Post-pandemic, Iowa now requires private insurance to offer some level of coverage for telehealth services as well.

It is important to note that insurance plans may have limitations on the number of mental health visits or the types of treatments that are covered. For example, your insurance plan may require pre-authorization for certain treatments, limit who you can see, or may require an audit or pre-authorization from the counselor after a certain number of sessions in a year.

Some insurance plans are exempt from this law, including:

- Some government plans and programs like Medicare

- Some state government employee plans may opt out of the parity requirements (like those covering teachers and employees of state universities)

If you are looking for a new insurance policy, here are some things you should consider if you want to use mental health benefits:

- Mental Health Coverage: The first thing you need to ensure is that the insurance plan covers mental health treatment. Many plans offer mental health benefits, but the specifics of what is covered can vary widely. Look for a plan that covers mental health services you need which may include therapy, psychological testing, behavior therapy, psychiatry, and substance abuse treatment.

- In-Network Providers: Another key consideration is the availability of in-network mental health providers. In-network providers have contracts with the insurance and have agreed to accept a certain rate of payment from the insurance company for their services, which can reduce your out-of-pocket costs. Check the plan’s provider directory online to make sure there are mental health providers in your area who are in-network. You can also call the member services number on the back of your card and ask for names of covered providers in your area.

- Out-of-Network Coverage: Even with in-network providers, there may be times when you need to see an out-of-network provider. Look for a plan that offers some coverage for out-of-network care, although you can expect to pay higher out-of-pocket costs for these services and you may have to submit the claims to insurance yourself.

- Copays, Deductibles, and Coinsurance: Pay attention to the plan’s copays, deductibles, and coinsurance rates, which will determine how much you’ll pay out of pocket for mental health services. Copays are a fixed amount you pay for each visit, while deductibles are the amount you must pay out of pocket before insurance coverage kicks in. Coinsurance is the percentage of the cost of care you’re responsible for after you’ve met your deductible. Lower copays, deductibles, and coinsurance rates generally mean lower out-of-pocket costs for mental health care.

- Preauthorization Requirements: Some insurance plans require preauthorization for certain mental health services, such as psychological testing, hospitalization or intensive outpatient treatment. Make sure you understand these requirements and how to obtain preauthorization to avoid unexpected expenses.

- Telehealth Services: Many mental health providers offer telehealth services, which can be a convenient and cost-effective way to receive care. Look for a plan that covers telehealth services, especially if you live in a remote area or have mobility or transportation issues.

If you are seeking mental health treatment, it is important to carefully review your insurance plan documents to understand what is covered and what your costs will be. You can also contact your insurance provider directly to ask specific questions about your mental health benefits and coverage, or speak with your company’s HR department.

We know health insurance can be confusing…

but don’t let that stop you from getting the help you need. There are so many resources available. If you are unsure where to start, you can call the number on the back of your insurance card to get a list of covered providers in your area.

If you are looking for mental health counseling please use the contact form or give us a call to get scheduled. You can also read more information about what insurance we accept here and view some FAQs about our services here.